Share this

I’ll often get lunch and a quick workout in one trip, and that was the case one early winter afternoon when I sat quietly with some chicken noodle. I recognized one of the personal trainers from my gym when he sat at the booth next to me, a young guy no older than 26-27. His back was towards me when a few minutes later a young woman came in with a big stack of paperwork and started spreading them out – the pitch was on! I tried my hardest to ignore them, but they were just too close. I started to pick up familiar terms: cash value, loans, tax-free… I was listening to the dreaded siren song of a life insurance saleswoman. Like a bad carnival attraction, now I was curious, and I started to eavesdrop to see how this ended up. See, I really wanted to publish an educational viewpoint about insurance, to keep most of my opinion and anger out of it. I was all set with that…then I sat down that day for lunch…

Nearly everyone will review and consider life insurance at some point and nearly the same amount will overpay for it. Through my career I’ve seen an incredible amount of people that are over-insured, in products they don’t need, paying too much, and don’t understand what they own. I want to cover some high level concepts about insurance and in the process warn you against some of the unnecessary products that are designed to be sold and not bought. If you stick with my story, I hope to leave you with a few rules to simplify life insurance, and also keep you from being ‘trapped’ by a bad sale.

Let’s start with a very basic concept: insurance is protection against bad things. We all encounter risk, some more than others, but it’s always lurking. The easiest way people understand insurance is through our cars – we can’t drive them without it. You don’t buy car insurance because you’re hoping for a great return on your investment, you get it so you can drive without fear of a huge repair bill. You pay a small amount each year to an insurance company, and their job is charge you enough to cover the much larger tab should you decide to run into your neighbor’s fence. Insurance companies do this through ‘risk pooling,’ basically grouping a bunch of people together, assigning a probability to one of them hitting the neighbor’s fence, and collecting enough of insurance premium to pay the expected fence bill.

A second insurance concept important to this discussion: When you pay your premium, you pay it in advance (you buy car insurance now so you can drive for the next 6 months). The money the insurance company collects sits in their account- it’s called ‘float.’ Float is the money (your premiums) the insurance company keeps until you make a claim. If they have one customer, that money is nice. Ten million customers? That’s a lot of float – they get to keep it, and all of the interest, as long as people pay their insurance premiums. Warren Buffett is the richest person for a reason: as of 2016 his company Berkshire Hathaway had about $89 billion of insurance float!

As I’ve written previously, Wall Street is very good at identifying opportunities for profit. If they sniff a dollar in your pocket, you better believe they’ll come up with a product that will help get that dollar out. The large insurance companies have created a vast ‘confusopoly’ of fancy sounding products, each with more complicated features than the last. Lots of bells and whistles attached to basic insurance to make you think you’re getting an amazing deal or generous return…but really just charges you more float.

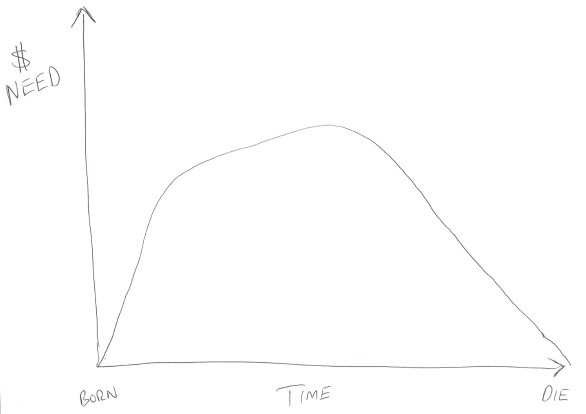

Here’s a rudimentary graph of life insurance needs, I sketched it myself – it’s a good thing I do finance for a living and not art:

As the graph shows, you’re born needing no life insurance, as you reach working age you need it to cover debt and dependents, and finally, your needs fade as you save money and your dependents become in-dependents. Pretty simple, right? You really only need life insurance for a certain period of time and that can be done relatively cheaply. There are exceptions, but they affect an extremely small percentage of people, so your graph is very likely to look just like this.

The concern is the ‘middle’ of the graph. It’s when your children are dependent on you to provide for them, it’s when you don’t have much saved, and it’s usually when you’re paying down big debts (like a mortgage or student loans). Term insurance was designed to do just that, it will provide a guaranteed death benefit for a ‘term,’ usually 20 or 30 years. Typically that’s more than enough time for you to pay down debt, save money, and get the kids to adulthood and off the books.

Life insurance can be an emotional purchase, who wants to ponder their mortality and assign numbers to it? Remember, fear and greed move markets, and fear and greed sell investments. What’s a better chance to exploit fear and greed than death insurance!?!

Enter the life insurance pitch. There are too many variations of products on the market to be specific, whole life, variable life, universal life, indexed life, etc…but the general pitch goes like this:

You: I need some life insurance because I just got married and we’re about to have a baby. My mortgage is $200k and I don’t really have any other debt, could I get a simple policy for $500k?

Insurance Salesperson (all prepared to sell FEAR): Great! Yes, I can help you get life insurance but $500k is not nearly enough!! After all, if you were to die prematurely, who would take care of your wife and child? I’ve done this calculation for you, and it shows you need at least $5 million of permanent life insurance to protect against all those years of lost income, pain, suffering…

You: But I have no other debt than the mortgage and we’ve saved up some money, plus my wife works and would continue to do so…

Insurance Salesperson (all prepared to also sell GREED): Plus, not only are you insuring against all these terrible scenarios, but did you know how great of an investment insurance can be? You can build up value in the policy just like savings, then loan it to yourself someday if you need the money, and it’s all tax-free!!!!

You: Why would I want to loan my own money back to myself? Why wouldn’t I just save that money and get the basic insurance I need?

Insurance Salesperson (completely ignoring the question): As you can see on this 100-page projection I’ve made for you, the performance of this life insurance policy will be way better off for you in the long run, then you can tell all of your peers that you’re too smart to be in the risky stock market, and by the way do you have any friends and family that I can call about this?….

Aaand…scene.

I obviously took some creative license with my dialogue, but ask any physician or attorney, they’ve probably heard some version of this pitch. Life insurance agents are told, and I’m paraphrasing, to go find people that make a lot of money and sell them lots of insurance. Some will dial the phone number of a local attorney’s office and continue, changing one digit, until they’ve reach every desk in the office. Agents are also trained to notice, and notice quickly, to exploit your emotions. If you’re fearful, they’ll pound on the projection that you’re not insuring enough. If you’re greedy, they’ll show you how much money you’ll make with their ‘special’ investment.

These guys are experts at sales; they will often present themselves as ‘financial advisors,’ or even worse, as just your friend looking to catch up over coffee. The best ones won’t lead with the insurance, even they know ‘insurance sales’ has a bad connotation. No, they’ll slow play you, making small talk, then asking about your overall goals and needs. These are wolves in sheep’s clothing: at the back end of the conversation, without fail, you will be presented with a permanent life insurance contract.

What isn’t included in their pitch? Whole life insurance can cost 6 to 10 times more than a similar term insurance contract, and you’re paying all that to have insurance when you need it the least. The agent gets paid a percentage of your (now larger) premiums, upfront, and in return for that you get a surrender charge on your money, i.e. – a penalty on your ability to get out of the contract. These will completely wipe out any value you’ve built if you try to get rid of the contract in the first decade. The insurance companies do this to protect their interests – after all, they just paid the agent a huge commission and have to make that up on the float. Now the insurance company has your float locked in, the agent gets a huge commission, and the result is you have a product you never understood, a product that doesn’t really do what it’s supposed to, and you have no easy exit. Studies have shown that nearly 80% of people regret purchasing these types of products!

A typical salesperson might object to term insurance by saying: ‘You want to pay for insurance and be left with nothing when you’re 60!??!’

Yes, that’s exactly what I’m saying.

If you’re 30 with a spouse and a 1 year-old, and you need $2MM of insurance now to protect your family against an untimely death, how much of that protection is required at age 60? Your 1 year-old is now 31. Your mortgage is probably long gone, or at least paid down significantly. And hopefully you’ve been saving for decades, enough that your assets far outweigh liabilities.

Why would you need all that life insurance at that age?

The real reason so many people end up with these contracts is simple: They were sold something they didn’t need by someone without their best interest in mind.

Don’t just take my word for it…here’s what Brett Arends, a columnist for Marketwatch, said in a March article when talking about his brief career as a life insurance salesman:

A friend wanted to buy a life-insurance policy that would protect the interests of his three young children if he should fall under the proverbial bus before they had all finished college. The aim of the policy was to cover their living costs and college expenses until they graduated.

His insurance costs were going to be high, because he was not in the best of health. The best way to meet his needs without costing him a fortune was to create a life-insurance policy with a declining payout as the children got older. It’s that simple. If he died early, his widow would be left to raise three children and send them all to college. If he died years later, she might only be left with one.

The needs declined, and sharply. So should the policy, and hence the cost.

But when I asked colleagues how to construct such a policy, they looked at me like I was nuts. First, the company didn’t even make such policies. And constructing one from multiple expiring policies was going to take a lot of time and effort. It just wasn’t worth it. In that time I could more constructively go and sell multiple big policies to other people.

And, second, why would I even do this? It was in my interest to sell my friend a $1 million policy that lasted all the way through to the third child’s graduation. Yes, it would cost him a lot more. But I’d get a much bigger commission as a result.

It would have been a total rip-off. But it would have been conventional enough that I could have defended it in any court or before any regulator if challenged.

In short, even if an agent knows what they should do for you, their companies don’t have the products to do it and their compensation will be much less if they did. Plus, they’re often representing the name on their business card, which means they’re not going to shop around for you. You’re simply going to be presented with that company’s product, which may be more expensive than a similar competitor. The entire industry is aligned to sell you something you don’t need. As Brett alludes, the situation screams unethical, yet remains just on the right side of legal.

I once had an agent that knew me, knew what I did for a living, and knew I was licensed to sell insurance…try to sell me insurance. I could have done the policy myself, signed it myself, and received the commission myself, but damnit he was going to give it a try anyway!

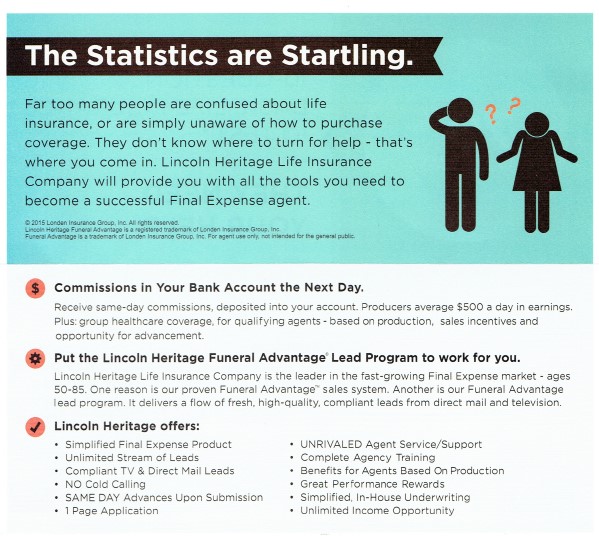

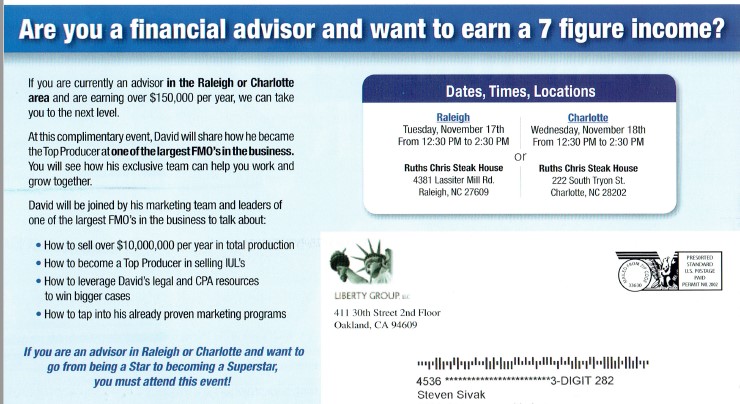

If you still don’t believe insurance is nothing but a massive sales contest, here are two recent ads I received in the mail:

These are pretty great, right? What do you notice? Not much talk about how to help people, or Term insurance, but lots of talk about how much money I could make! I can use the ‘Funeral Advantage Lead Program’ (admit it, you really want to know how that program works) to boost my sales, or go from a ‘Star to a Superstar’ and earn a 7-figure income selling Indexed Universal Life (IUL). I thoroughly enjoy getting ads like these in the mail for their entertainment value (Superstar!), but the shameful truth is right there to see: the emphasis is on selling you expensive products without any regard for what you need. One of the bullets even points out ‘Benefits for Agents based on Production.’ If you sit down across from one these guys and his family’s health insurance depends on him selling you one of these policies, what chance do you think you have to suggest something else?

To make this story a bit more real: I once had an 80 year-old couple make a special trip to my office to talk (they really didn’t drive anymore). They had saved a small amount of money, but they had more or less outlived it and their situation was pretty dire, the conversation was a difficult one and involved some tears. They were quite scared.

I had counseled them several times that they had to cut costs as best as possible. Interest rates were very low, their fixed income investments just couldn’t produce enough to pay for their current budget. After a half hour of reviewing their entire budget and various expenses, the wife revealed that they had a life insurance contract. When I asked for more details I realized this couple, who were considering selling their house and not traveling anymore to see their grandkids, were still making payments on a life insurance contract! Needless to say, life insurance premiums are extremely expensive when you’re in your 80s! I was stunned, I told them to stop making the payments immediately and I asked them why they hadn’t stopped sooner. They admitted that they were only doing what ‘their guy’ had recommended each time the policy was up for renewal.

That brings us back to my lunch that day…

After listening to her pitch, including a cringe-worthy moment where she asked if he could give her the names and numbers of anyone else he ‘really cared about’ so she could share the product with them, I couldn’t take it anymore. I walked over to the table, asked if they were talking about life insurance, and promised him that I would catch up with him later. Days later, I did, and told him everything I’m telling you.

Now since I can’t be sitting next to everyone at lunch, here’s my brief life insurance action plan to save you from the wolves!:

- Assess your life insurance based on ‘the middle’ of your life. How much debt are you carrying? Do you want to put the kids through college? Do both spouses work? A reasonable amount will make sure all debts are paid, maybe the kids’ college and potentially another chunk goes towards income replacement. Years later, when the kids are gone and house is paid off, that number should go way down.

- Price out term policies, trying to tie your dates closely to when you feel the kids will be ‘off the books.’

- Have a professional who is NOT a life insurance agent and does NOT receive commissions give you an opinion. Even some term policies have gadgets in them to make you pay more.

- Get life insurance to prevent bad things, but don’t confuse it with an investment, no matter how persistent the salesperson. Buy cheap insurance and invest what’s left, the returns over decades will far outweigh any return you could receive through insurance.

This post originally appeared Innovate-Wealth.com

|

About Steven Sivek Over the past 10 years, Steve Sivak has worked with high net worth individuals in all situations and through several market cycles. Client frustrations with the ‘Big Bank’ model of the business led him to want to improve the experience. Steve created Innovate Wealth with the vision to refocus the business away from a product sales culture and back to the clients, their education, their behavior, and do it all at a more affordable cost.

|

Share this

Subscribe by email

You Don't Need Life Insurance Until You Have This

Life Insurance